Cold storage infrastructure is expanding faster than many industrial sectors.

Food logistics networks are scaling. Pharmaceutical cold chains are becoming more complex. Online grocery fulfilment continues pushing refrigerated warehousing demand higher across both mature and emerging markets.

That growth is changing how businesses think about storage inside cool rooms.

Shelving is no longer viewed as a basic fit-out component. In many facilities, it directly affects storage density, inventory accessibility, hygiene compliance, airflow efficiency, labour productivity, and long-term operating costs.

The broader cold chain logistics market reflects that shift. Global cold chain logistics is projected to grow from USD 496.8 billion in 2026 to USD 1.48 trillion by 2035, representing a CAGR of 12.97%.

At the same time, global cold storage capacity is expected to reach approximately 1.35 billion cubic metres by 2030.

Those numbers point to a much larger structural trend.

More refrigerated warehouses mean more cool rooms. More cool rooms create greater demand for storage systems that maximise capacity without compromising workflow, food safety, or operational efficiency.

For businesses operating temperature-controlled facilities, storage infrastructure is increasingly becoming part of the productivity equation rather than simply a storage expense.

Cold storage has evolved from a specialised warehousing segment into core infrastructure supporting global food supply chains, healthcare systems, retail distribution, hospitality operations, and pharmaceutical logistics.

Capacity growth has accelerated accordingly.

The International Institute of Refrigeration reported that global cold storage capacity reached 719 million cubic metres in 2020, increasing 16.7% compared to 2018.

That growth trajectory has continued post-pandemic as governments and private operators increase investment in food security, pharmaceutical resilience, and temperature-controlled logistics infrastructure.

Large-scale operators are expanding aggressively.

The Global Cold Chain Alliance stated that its members now operate more than 8.16 billion cubic feet of temperature-controlled warehouse space globally.

Additional GCCA reporting showed refrigerated warehouse capacity among major cold storage providers increased by more than 10% in 2025 alone.

The implications extend beyond warehouse construction.

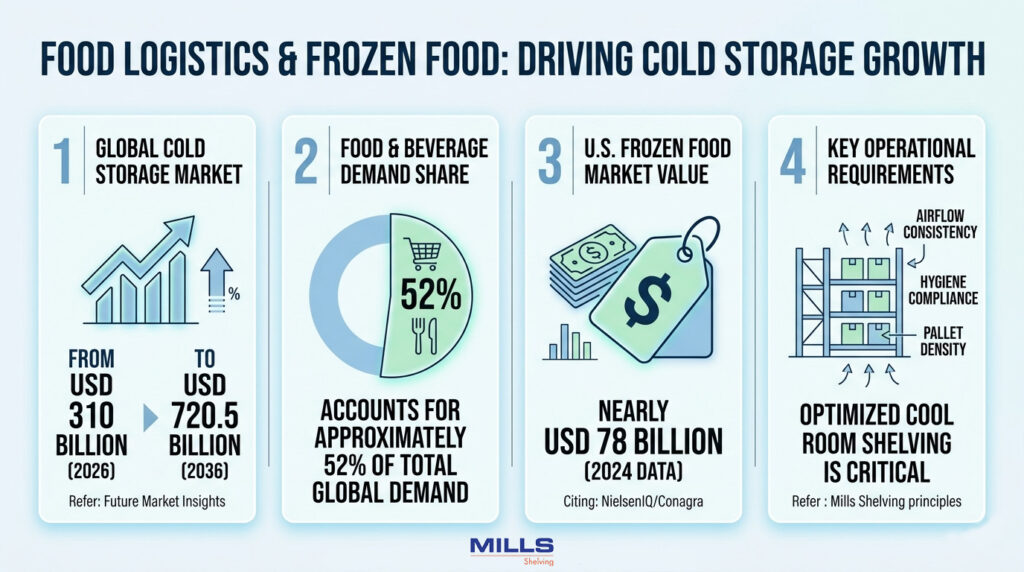

As facilities scale vertically and operators attempt to improve storage density, internal infrastructure requirements also become more demanding. Shelving systems must support heavier inventory loads, withstand moisture exposure, improve airflow circulation, and maintain hygiene compliance under constant operational pressure.

Many operators are also moving away from fixed layouts.

Facilities increasingly need adaptable storage systems capable of handling seasonal inventory fluctuations, changing SKU counts, and evolving workflow requirements. That shift is one reason modular and adjustable cool room shelving systems are becoming more common across food service, hospitality, and logistics facilities.

Food remains the single largest driver of global cold storage demand.

The growth of online grocery fulfilment, prepared meal distribution, quick-service restaurants, frozen food consumption, and large-scale food logistics networks continues to increase pressure on refrigerated infrastructure globally.

Future Market Insights projects the global cold storage market will grow from USD 310 billion in 2026 to USD 720.5 billion by 2036.

The food and beverage sector accounts for approximately 52% of total global cold storage demand.

That concentration matters because food storage environments create unique operational requirements compared to conventional warehousing.

Inventory turnover is faster. Hygiene standards are stricter. Airflow management becomes more important. Shelving durability is constantly tested through moisture, temperature fluctuations, cleaning chemicals, and high-frequency handling.

Frozen food demand continues to reinforce these pressures.

NielsenIQ-backed data from Conagra’s Future of Frozen Food 2024 report showed the U.S. frozen food market is now worth nearly US$78 billion.

That growth is flowing directly into warehousing requirements.

Operators handling frozen inventory are increasingly focused on:

These operational demands are pushing many businesses to rethink how shelving systems are configured inside cool rooms.

At Mills Shelving, one of the more common operational issues businesses encounter is underutilised vertical space. Many facilities still rely on layouts designed years earlier when SKU counts, fulfilment volumes, and inventory requirements were significantly lower.

Modern refrigerated environments increasingly require shelving systems that can adapt as inventory requirements evolve.

That is one reason many operators now spend more time evaluating storage configuration before installation, particularly around load ratings, airflow clearance, corrosion resistance, and accessibility. Businesses comparing different systems often start with practical considerations such as shelf adjustability, hygiene compliance, and long-term maintenance requirements before reviewing broader operational fit. Resources such as this guide on how to choose the right cool room shelving have become increasingly relevant as facilities become more operationally complex.

Food logistics may dominate overall cold storage demand, but pharmaceutical distribution is becoming one of the fastest-growing sectors within the broader cold chain industry.

Temperature-sensitive medicines, biologics, vaccines, and specialty pharmaceuticals are driving major investment into highly controlled refrigerated storage environments.

The pharmaceutical cold-chain logistics market is projected to reach USD 44.1 billion by 2033.

At the packaging level, the pharmaceutical cold-chain packaging market is forecast to increase from USD 9.26 billion in 2025 to USD 26.41 billion by 2034.

The long-term trend is even more significant.

MetLife Investment Management reported that more than 50% of new medicines are expected to require cold storage by 2032.

That fundamentally changes storage requirements inside pharmaceutical facilities.

Pharmaceutical cold rooms often require:

Shelving systems operating in these environments need to support both compliance and operational efficiency simultaneously.

Small inefficiencies inside pharmaceutical storage environments can create larger downstream risks around spoilage, stock rotation, compliance breaches, or retrieval delays.

As a result, pharmaceutical operators are increasingly prioritising shelving systems that are easy to clean, corrosion-resistant, modular, and capable of supporting structured inventory management processes.

The broader refrigerated warehousing sector is now under substantial infrastructure pressure.

Capacity demand continues rising faster than supply in many regions, particularly in urban distribution markets where land constraints and construction costs are already high.

The International Institute of Refrigeration also reported that U.S. refrigerated warehouse capacity increased from 104.8 million cubic metres in 2023 to 113 million cubic metres in 2025.

Even with expansion underway, operational pressure remains high.

CBRE estimates the U.S. cold-chain logistics market is now worth approximately US$90 billion.

Its 2025 Midwest Cold Storage report also noted that much of the region’s existing refrigerated infrastructure is ageing and operationally inefficient.

That pattern is not unique to North America.

Across multiple global markets, operators are increasingly retrofitting older cold rooms rather than constructing entirely new facilities due to rising construction costs, planning constraints, and infrastructure limitations.

For shelving providers, that creates a different type of demand.

Many retrofit projects focus less on adding floor area and more on extracting higher storage performance from existing space. In practical terms, that often means increasing shelf density, improving accessibility, reducing dead space, and creating layouts better aligned with modern inventory workflows.

In older facilities especially, storage optimisation can often deliver faster operational gains than expanding warehouse footprint itself.

Australia’s cold storage market is expanding, although available capacity still remains comparatively constrained relative to population growth and logistics demand.

JLL reported that Australia currently has only 0.4 cubic metres of refrigerated warehouse space per urban resident.

For comparison, some international markets operate with significantly higher refrigerated storage capacity per capita. That gap is becoming more visible as online grocery fulfilment, pharmaceutical distribution, and food logistics networks continue scaling across Australian cities.

JLL also estimates Australia will require an additional 750,000 square metres of cold storage floorspace by 2030.

The infrastructure buildout is already underway.

The challenge for many operators is not simply adding capacity.

It is adding usable capacity efficiently.

Cold rooms are expensive to build, expensive to operate, and expensive to expand. Every square metre matters. Businesses are increasingly looking for ways to improve storage density inside existing facilities before committing to larger infrastructure projects.

That is driving stronger interest in modular storage systems capable of adapting alongside operational growth. In practice, many operators now prioritise shelving flexibility, airflow efficiency, cleanability, and long-term durability as part of broader warehouse planning decisions rather than treating shelving as a final fit-out item.

Cold storage expansion across the Asia-Pacific is occurring unevenly.

Some markets are struggling with ageing infrastructure and supply shortages. Others are investing aggressively to modernise food distribution and pharmaceutical logistics networks.

Japan highlights both sides of the problem.

GCCA reporting showed that major Japanese cold storage markets are operating at near or above full capacity.

At the same time, approximately 33% of Japan’s cold storage floor space is now more than 40 years old.

That combination creates operational pressure quickly.

Older facilities often struggle with energy efficiency, layout optimisation, automation compatibility, and modern inventory throughput requirements. Retrofitting becomes increasingly necessary, particularly where warehouse expansion is restricted by urban density or land constraints.

Singapore is experiencing a different growth dynamic.

Its cold-chain perishables market is expected to double by 2034.

Population density, food import dependency, and rising eCommerce demand continue pushing investment into temperature-controlled infrastructure across the region.

Emerging markets are also accelerating investment.

Separately, the Philippines reached 739,000 pallet positions of cold storage capacity in Q2 2024, while cold storage demand continues growing between 10% and 15% annually.

Much of this growth is tied directly to food security, agricultural logistics, retail expansion, and healthcare distribution.

As more facilities come online across Asia-Pacific, shelving infrastructure requirements are becoming more sophisticated. Operators increasingly need storage systems that can handle high humidity, frequent cleaning, inventory rotation pressure, and changing product mixes without compromising operational efficiency.

Storage density has become one of the most important performance metrics inside refrigerated environments.

Cold storage construction costs are substantially higher than standard warehousing. Operating costs are higher, too. Cooling unused space becomes an expensive inefficiency very quickly.

As a result, operators are increasingly redesigning layouts to improve storage output within the same physical footprint.

Modern cold storage facilities increasingly use automation to reduce aisle widths and improve inventory density.

High-bay automated cold storage warehouses can also reduce building energy consumption by around 20%.

Those efficiency gains matter because refrigeration costs compound over time.

Every additional cubic metre being cooled carries long-term operational cost implications. Improving vertical storage utilisation and reducing wasted aisle space can significantly improve warehouse economics across the life of a facility.

That is changing how shelving systems are specified.

In many projects, businesses are now prioritising:

This is one reason adjustable and customisable cool room shelving has become increasingly important for facilities expecting inventory requirements to evolve over time.

At Mills Shelving, flexibility is often one of the biggest differentiators between short-term storage planning and long-term operational efficiency. Facilities rarely remain static for years. Product categories change. SKU counts increase. Picking workflows evolve. Fixed layouts often become operational bottlenecks much faster than businesses initially expect.

Labour availability is becoming one of the defining operational challenges across cold storage globally.

Refrigerated facilities are physically demanding work environments. Staff turnover is often higher than in conventional warehousing. At the same time, fulfilment speed expectations continue increasing.

Automation is increasingly viewed as the long-term solution.

The food and beverage automated storage retrieval system market is projected to grow from USD 1.67 billion in 2026 to USD 3.91 billion by 2035.

The same research also highlighted how automated cold storage systems improve inventory accuracy while reducing labour dependency.

Some of the world’s largest cold chain operators are already moving heavily in this direction.

Lineage Logistics now operates 82 automated cold storage warehouses globally.

Automation changes storage design requirements substantially.

Warehouse layouts increasingly need compatibility with:

Traditional shelving approaches often struggle to support those environments efficiently.

The broader shift toward automation is also pushing businesses to think more strategically about future scalability during initial fit-outs. Many facilities now evaluate shelving systems based not only on current operational requirements, but also on their ability to support future warehouse upgrades.

Cold storage facilities are among the most energy-intensive building types in the industrial sector.

The National Renewable Energy Laboratory reported that refrigeration systems can consume more than 70% of total electricity usage inside refrigerated warehouses.

Globally, refrigeration accounts for approximately 15% of total electricity consumption.

The environmental impact is substantial as well.

The food cold chain contributes roughly 1% of global greenhouse gas emissions.

That combination of rising energy costs and emissions pressure is reshaping how facilities are designed, upgraded, and operated.

Operators are increasingly investing in:

Thermal energy storage systems can reduce cold storage energy costs by up to 50%.

Large operators are already implementing these changes at scale.

Americold reported that LED upgrades reduced annual energy use by more than 2 million kWh across its facilities.

Energy efficiency now influences shelving decisions more than many businesses realise.

Poor shelving layouts can restrict airflow, create temperature inconsistencies, increase compressor workload, and reduce overall operational efficiency inside cool rooms.

Storage design is increasingly becoming part of a broader sustainability strategy rather than simply a warehouse organisation.

As refrigerated infrastructure expands globally, demand for shelving and racking systems is increasing alongside it.

The warehouse racking market is also forecast to reach USD 14.63 billion by 2034.

That growth reflects broader changes occurring across warehousing itself.

Storage systems are no longer judged purely on basic capacity. Businesses increasingly evaluate shelving around operational efficiency, hygiene standards, airflow optimisation, scalability, durability, and lifecycle cost.

Inside cool rooms, specifically, shelving systems increasingly need to support:

Cost considerations remain important as well.

Operators are balancing upfront installation costs against long-term operational efficiency, maintenance requirements, durability, and future scalability. Many businesses now spend more time evaluating lifecycle value rather than simply comparing initial purchase pricing.

For facilities planning new installations or upgrades, resources such as this cool room shelving price guide are becoming increasingly useful for understanding how material selection, shelf configuration, load requirements, and layout complexity influence overall project costs.

Cold storage infrastructure is expanding rapidly across food logistics, pharmaceuticals, retail, hospitality, and eCommerce fulfilment.

That growth is increasing pressure on refrigerated facilities to improve storage density, workflow efficiency, hygiene compliance, and operational scalability.

Shelving systems are no longer viewed as basic storage components. They now directly affect labour efficiency, inventory accessibility, airflow, maintenance requirements, and long-term operating costs.

At Mills Shelving, we are seeing more businesses prioritise durable, modular, and higher-density cool room shelving systems

that can adapt as inventory and operational requirements change.

For many operators, improving storage efficiency inside existing cool rooms is becoming more practical and cost-effective than expanding the warehouse footprint.